- Winter 2024: BENEFITS

Disability

Report objectives

The objective of this report is to provide a broad view of our current metrics for our disability programs and provide an overview of the current environment surrounding disability claim administration. Our compliance and data analytics teams collaborated to configure JURIS claims data into a Sedgwick “state of the line” report intended to compare our trends with other relevant industry studies.

data parameters

Data is based on the calendar year, January through December, for each reporting year.

Key observations

Short-term disability (STD) incident rates decreased in 2023 from 12.6% to 10.9%. The primary driver of this was an 80.9% decrease in COVID-19 volumes in 2023. Excluding COVID-19 volumes, incident rates stabilized in 2023, showing a slight increase from 10.6% to 10.7%.

Pregnancy was the top diagnostic group for new STD claims in 2023, making up 14.6% of the claims; however, mental and substance new claims increased by 4.5% in 2023, making up 12.2% of claims.

Mental and substance incident rates increased in 2023 after decreasing from the year prior. Incident rate specific to mental and substance increased 3.9% year-over-year, with anxiety incident rates increasing 2.1%.

Average duration on STD claims increased in 2023, primarily due to the large decrease in the volume of COVID-19 claims. The volume dropped by more than 83% while duration increased by 40%. Durations for non-COVID claims decreased by 0.3% in 2023.

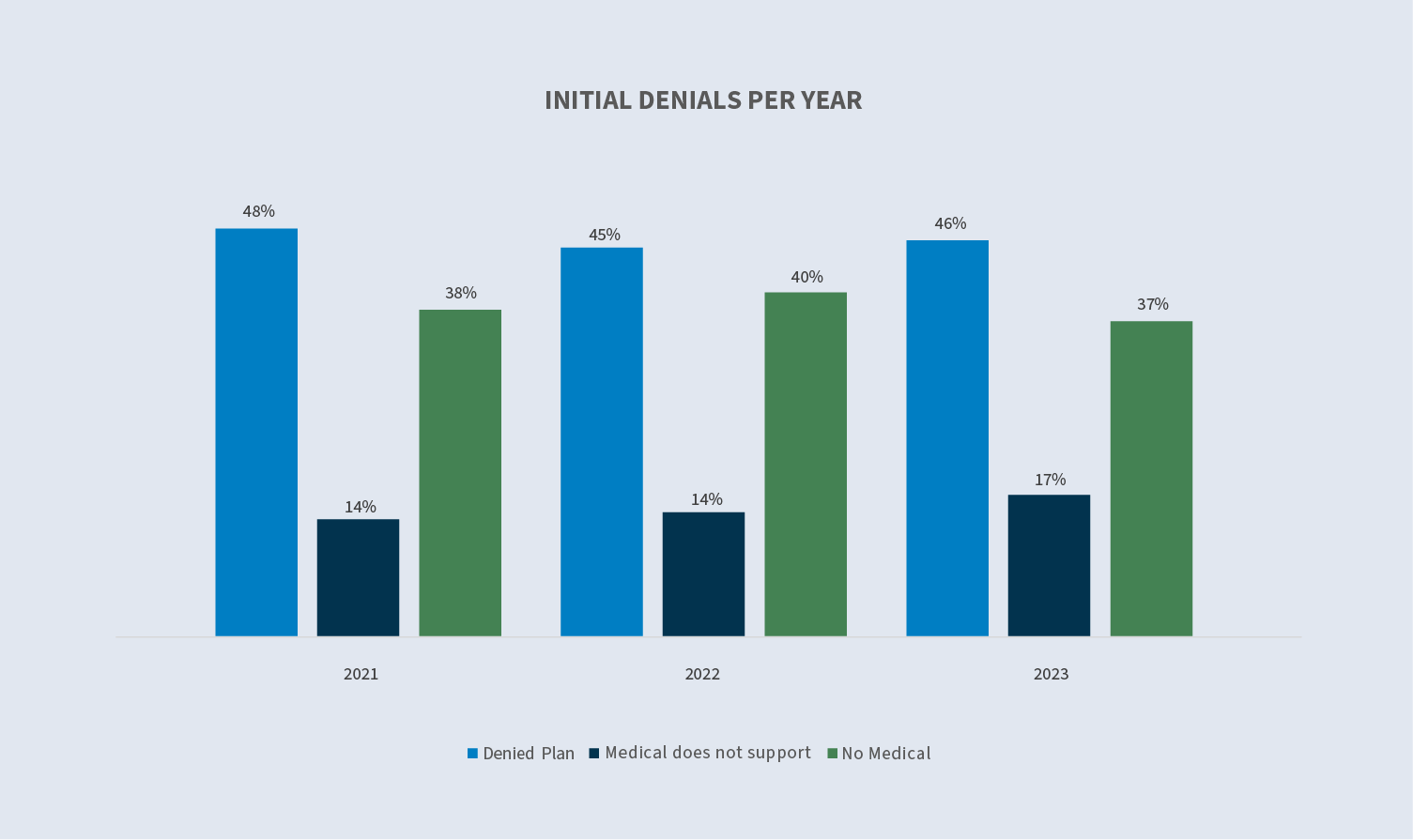

Initial denial rate on STD in 2023 decreased for the first time in three years, dropping from 19.3% in 2022 to 18.2% in 2023. Failure to submit medical information decreased 3% compared to 2022, while denials due to plan and medical not supporting both increased. Denials due to insufficient length of service decreased slightly, from 2.1% to 1.9%.

Long-term disability (LTD) claims volumes increased 2.3% from 2022 to 2023, while open status volumes continued their declining trend.

Short-term disability

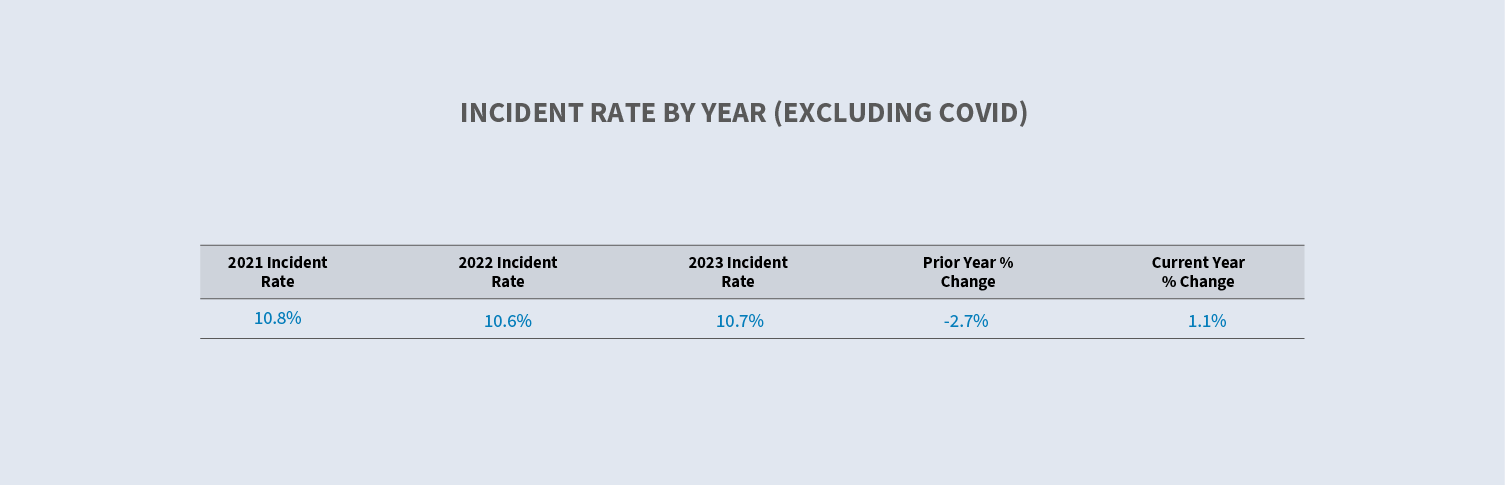

Incident rates by year

The large decrease in COVID claims caused our incident rates overall to decrease more than non-COVID claims.

With COVID removed, there was a slight increase in 2023. The incident rate was 10.8% in 2021, 10.6% in 2022 and up to 10.7% in 2023.

Diagnostic groups by percent of total

COVID claims were less than 3% of the total new STD claim volume in 2023 — down from 17.2% in 2022. This sharp decrease caused other diagnostic groups to make up a larger percentage of the whole, despite decreasing in volume and incident rates from 2022 to 2023. Mental and substance incident rates remained flat from 2021 to 2002 while increasing to 12% in 2023.

Regarding mental health, anxiety rates rose significantly early in the pandemic. This was driven by uncertainty about the pandemic and general worry from employees regarding their health and financial well-being. From 2019 to 2020, the anxiety incident rate increased 19.2% and remained high throughout 2021. In 2022, the anxiety incident rate decreased to 12.3%. Anxiety still makes up a larger portion of all mental and substance claims than pre-pandemic, at 44.8%, but is trending back down.

Average total days approved

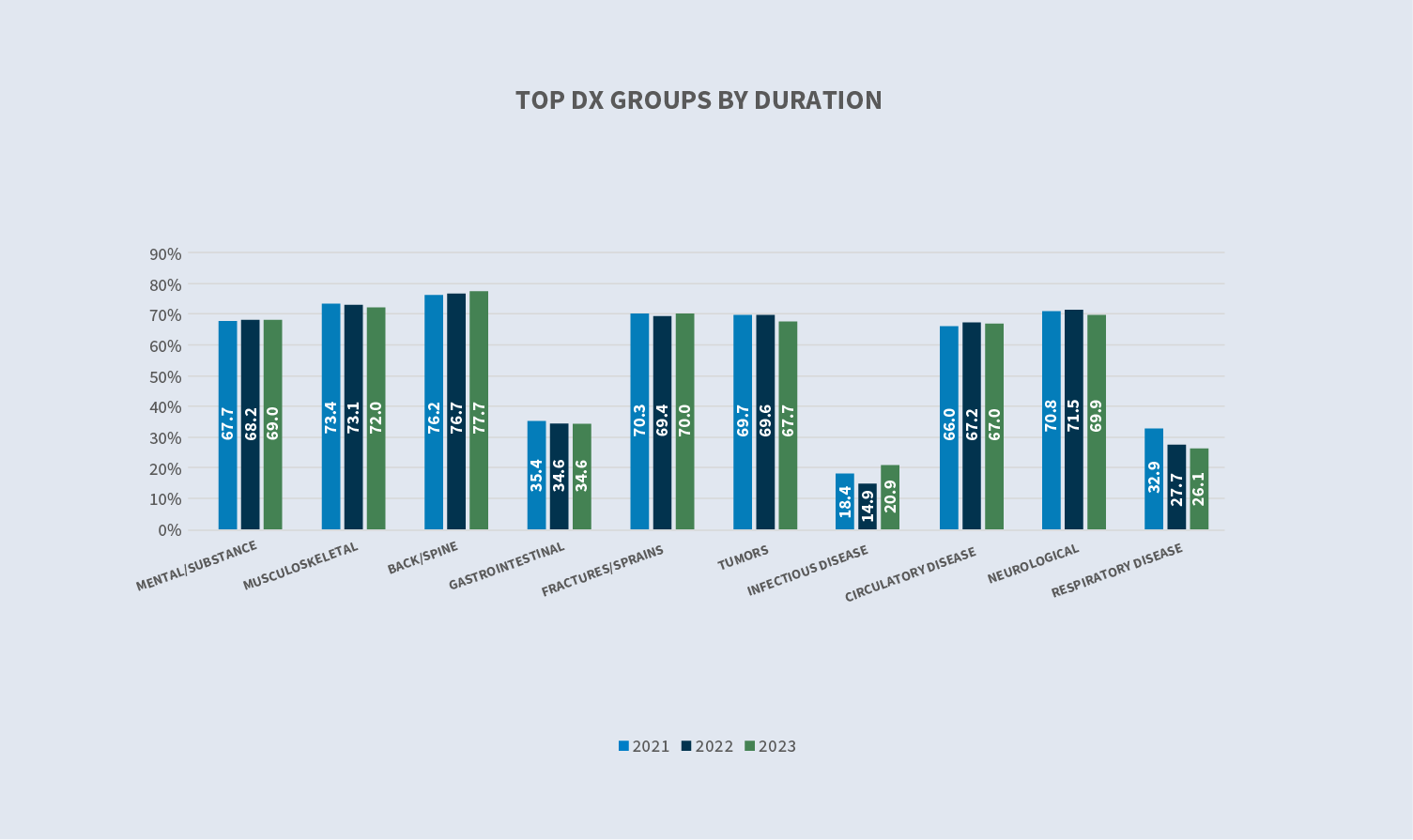

Overall, STD durations increased 13.3% from 2022, driven by the decrease in COVID claims. COVID claims have significantly lower durations than non-COVID claims — at only 20.9 days in 2023. With less claims of shorter duration, the overall average approved days increased. Durations without COVID claims included generated a dip of 0.3%, going from 58.0 days in 2022 to 57.9 days in 2023.

Outside of COVID claims, durations for all the other diagnostic groups within the top 10 are within 1% of 2022 with the exception of neurological claims and tumors claims, which decreased 2%. The other groups within the top ten that increased from 2022 are mental and substance (1.2%), back and spine (1.3%), and fractures (1%).

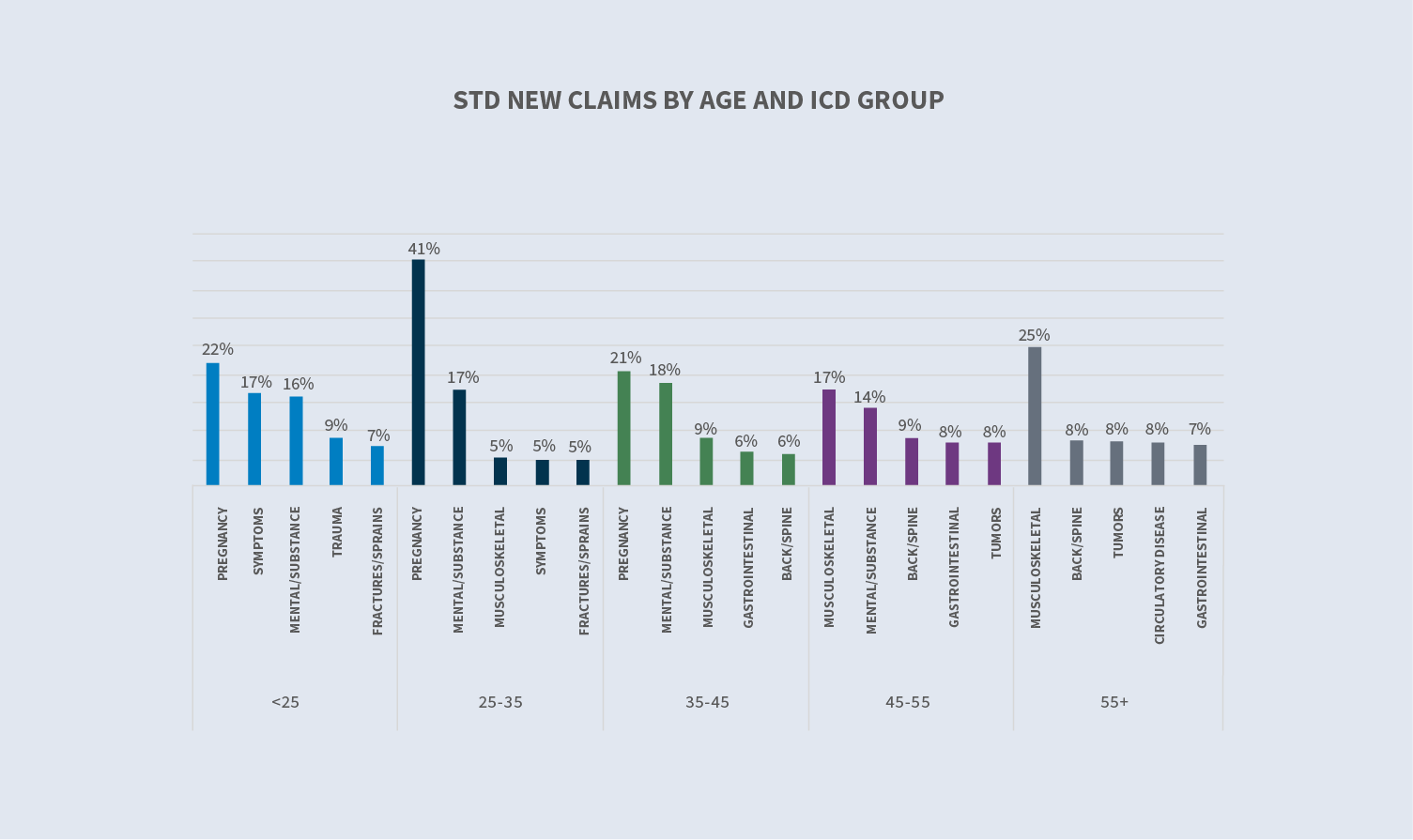

New claims by age

The age distribution of new STD claims reported in 2023 was stable compared to 2022. Claims filed by employees over 55 increased in 2023 compared to 2022 and 2021. For employees 25-35, there was no notable volume change in 2023 compared to 2022.

Claim closure reasons

The age distribution of new STD claims reported in 2023 was stable compared to 2022. Claims filed by employees over 55 increased in 2023 compared to 2022 and 2021. For employees 25-35, there was no notable volume change in 2023 compared to 2022.

Of the claims resolved in 2023, 21% were due to exhaustion of benefits. Resolved claims due to an employee death made up 0.6%, while 77.7% of resolved claims were due to the employee returning to work, a decrease when compared to 2022 (82%.)

Volumes by industry

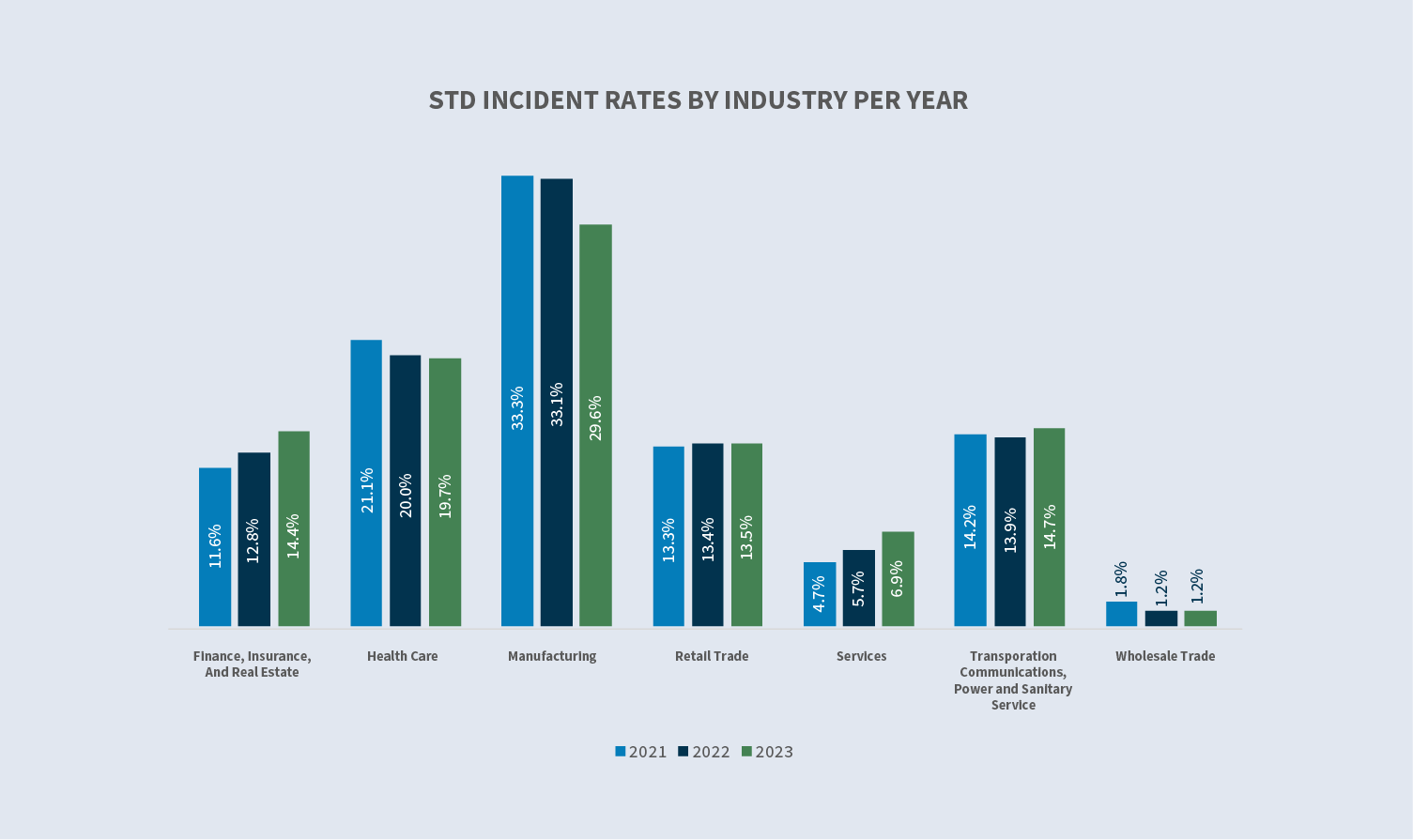

Every industry saw an increase in claim volumes when the pandemic hit in 2020, which continued for most industries in 2021. In 2022 and 2023, volumes reversed with decreases in healthcare, transportation, communication, power, sanitary services and wholesale trade. The industry groups where volumes increased are primarily driven by new business.

For incident rates by industry year-over-year, significant increases occurred in financial, insurance and real estate (12.8% in 2022 and 14.4% in 2023). Services increased from 5.7% in 2022 to 6.9% in 2023. Retail remained flat while the other groups decreased.

Incident rates by diagnostic group

While mental and substance volumes remain in the top five diagnostic groups for all industry groups, they are the leading cause of disability in transportation, communications, power and sanitary services. The incident rate decreased slightly for this group, from 2.7% in 2022 to 2.6% in 2023. Other industries showed a slight increase in incident rates for mental and substance.

Long-term disability

New claim volume

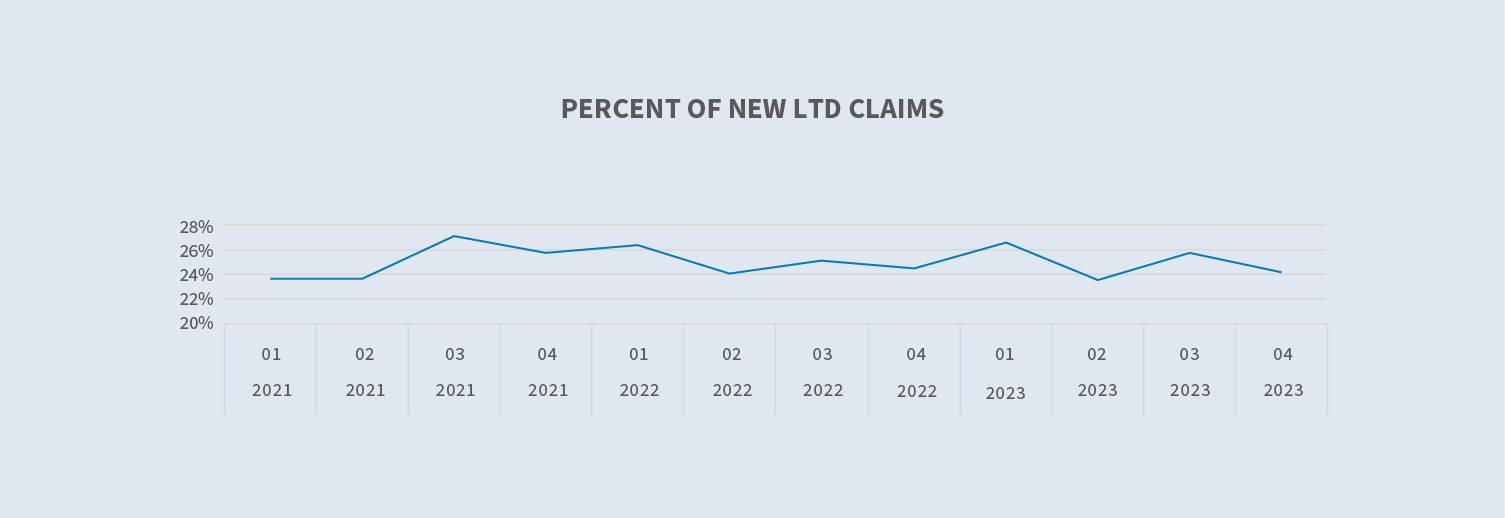

The open status volume of LTD claims continues to trend down, similar to what we have seen for the past three years.

Future considerations

Mental health provider shortage

According to the Psychiatric Times, the supply of mental health providers has been decreasing.

The Association of American Medical Colleges (AAMC) reports this number could be as high as 31,000, and 150 million Americans live in areas short on mental health professionals. If employees struggle to find appropriate care or have long wait times to see a provider, this could lead to changes in approval/denial rates or an increase in mental health claim durations.

A consideration for employers is to review their short-term disability plan, specifically any provisions for treating with a mental health professional. A study on Bank of America showed that by expanding the definition of an appropriate provider to include clinical psychologists and psychiatric nurse practitioners, the mental health denial rate decreased from 10.9% to 3.7%.

Long-haul COVID

Research suggests that between one month and one year after having COVID, 1 in 5 people aged 18 to 64 has at least one medical condition because of COVID. Among people 65 and older, 1 in 4 has at least one medical condition that might be due to COVID. The Centers for Disease Control and Prevention recently published that overall, 1 in 13 adults in the U.S. has “long COVID” symptoms.

The most commonly reported symptoms of long-haul COVID include:

- ∙ Fatigue

- ∙ Symptoms that get worse after physical or mental effort

- ∙ Fever

- ∙ Lung (respiratory) symptoms, including difficulty breathing or shortness of breath and cough

Long-term COVID is becoming an increasing cause of disability and accommodation requests.

Sedgwick began tracking when physicians certify a claim as long COVID in October 2022. Approximately 0.9 claimants per 100 employees reported a long COVID STD claim; however, we are only capturing long COVID when it reaches severity requiring absence from work and a physician identifies the claim as long COVID on the medical paperwork.

There is not a significant difference in long COVID claims filed by age, with employee 35-44, 45-54 and 55 and up all reporting claims at around the same rate.

Expansion of paid leave policies

Paid leave provides financial support (and sometimes job protection) when a new child or a personal or family care need requires an employee to take time away from work. Partially due to after-effects of COVID, employers and politicians better understand how necessary it is to provide paid leave to workers in support of them and their families. Although there is currently a task force in Congress working on a bipartisan federal solution, it is not likely that a federal paid leave option will be passed based on Congress’ current make-up. Therefore, states continue to establish and expand paid leave programs.

Here is a list of recent implementations and expansions:

Washington Paid Family and Medical Leave (WA PFML): Effective Jan. 1, 2025, any interested party will have access to certain records and information related to an employee’s paid family or medical leave claim, including the type of leave being taken, the duration of the leave and whether the employee was approved for and paid benefits. This Washington amendment defines “interested party” as a current employer, a current employer’s third-party administrator or an employee.

California Paid Family Leave (PFL) and State Disability Insurance SDI: For PFL and SDI claims beginning on or after Jan. 1, 2025, individuals who earn 70% or less of the state average quarterly wage (SAWW) will receive a benefit of up to 90% of the average weekly wage (AWW). Individuals who earn more than 70% of the state average quarterly wage will receive a benefit of up to 63% of AWW.

Maryland has enacted a Family and Medical Leave Insurance Program on April 9, 2022, effective Jan. 1, 2026.

Delaware has enacted the Delaware Healthy Families Act on May 10, 2022, effective Jan. 1, 2026.

Minnesota has enacted a Paid Family and Medical Leave Act on May 25, 2023, effective Jan. 1, 2026.

Maine has enacted a Paid Family and Medical Leave Act on July 11, 2023, effective May 1, 2026.

New York’s governor has proposed an increase in New York disability benefits to match the paid family leave benefit for the first 12 weeks of medical leave. Eligible employees would receive 67% of their AWW, capped at 67% of the SAWW, once fully phased in after five years. As this is a proposal, there is no implementation date.

Recent state programs have implemented a two-part (and sometimes three-part) formula, providing a higher percentage of wage replacement to lower-wage workers. This was done in the hopes of supporting people who are more financially insecure. This trend started with Washington providing low-wage earners 90% of their earnings. Minnesota and Maryland will do the same when their benefits take effect in 2026.

States with multi-part formula and the percentage of wage replacement that they offer lower-wage earners:

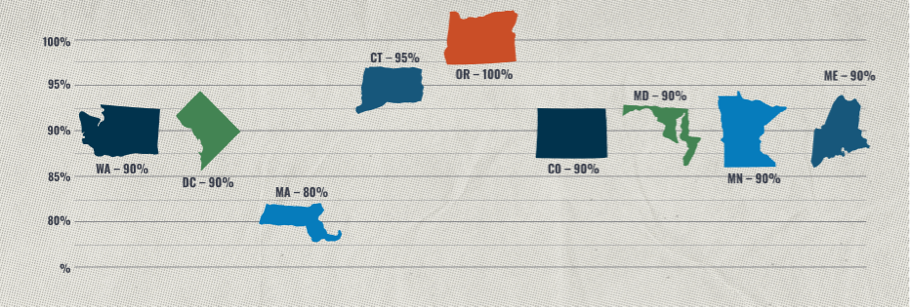

Generally, the definition of family member has trended to be more inclusive. Recently enacted laws extend the definition of family member beyond parents, spouses and children to include grandparents, grandchildren, siblings, parents-in-law and domestic partners. More importantly and more generously, in six states, family also includes a person “to whom the worker is related to by blood or affinity.” The “blood or affinity” family member definitions are applicable in Washington PFML, New Jersey Family Leave Insurance (NJ FLI), Connecticut FMLA and Paid Leave, California Family Rights Act (CFRA), Paid Leave Oregon and Colorado FAMLI. Interestingly, both Maryland and Delaware have both chosen to not follow the trend of this expanded family member definition. Minnesota and Maine continue with the “blood or affinity” relationship as part of their PFML programs.

Upcoming implementations and likely new states

2023 was the first year that two states implemented plans simultaneously. Specifically, Oregon Paid Leave benefits began Sept. 3, 2023, and Colorado FAMLI benefits began Jan. 1. After that, we have our first triple implementation: Delaware, Maryland and Minnesota, which will all roll out on Jan. 1, 2026. Maine is slightly behind this first grouping, implementing on May 1, 2026. That means there will be four new paid family and medical leave programs going live in 2026.

These states will not be the last. Based on the current make-up of the legislatures and governorships, it is likely programs will pass in Vermont, Michigan and New Mexico. Many other states continue to propose legislation and will likely try again as they have for the past few years.